Executive summary

This Winter interim Forecast lifts the outlook for growth and slightly lowers the inflation projections. Growth for 2022 is now estimated at 3.5% in both the EU and the euro area. GDP is projected to expand by 0.8% in 2023 and 1.6% in 2024 (0.9% and 1.5% in the euro area). Headline inflation is forecast to fall from 9.2% in 2022 to 6.4% in 2023 and 2.8% in 2024 in the EU. In the euro area, it is projected to decelerate from 8.4% in 2022 to 5.6% in 2023 and to 2.5% in 2024.

Since autumn, the EU economy has seen a number of positive developments. The European gas benchmark price has fallen below its pre-war level, helped by a sharp fall in gas consumption and continued diversification of supply sources. With hindsight, the resilience of households and corporations has been impressive. Despite the energy shock and ensuing record high inflation, the slowdown in the third quarter turned out milder than previously estimated and in the fourth quarter, the EU economy managed a broad stagnation, instead of the 0.5% contraction expected in autumn. Labour markets have also continued to perform strongly, with the unemployment rate in the EU remaining at its all-time low of 6.1% in December. Three months of falling inflation rates confirm that, as projected in autumn, the peak is now behind. Finally, economic sentiment has continued improving, suggesting that economic activity will avoid a contraction also in the first quarter of 2023. The EU economy is thus set to narrowly escape the recession that was pencilled in back in autumn.

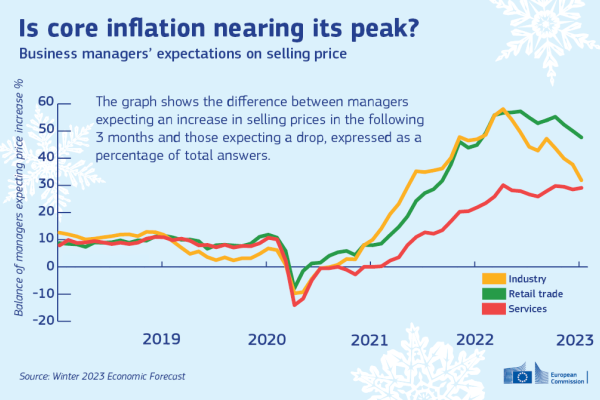

Yet the EU economy is still beset with challenges. Core inflation increased further in January. Consumers and businesses continue to face high energy costs and with more than 90% of the core items in the HICP basket registering above-average price increases, inflationary pressures are still broadening. Monetary tightening is therefore set to continue, exerting a drag on investment. Weakness in consumption is set to persist in the near term as inflation keeps outpacing nominal wage growth. Finally, the external environment is expected to continue providing little support to the EU economy.

All in all, recent developments do not warrant a substantial upward revision to the growth profile projected in autumn for 2023 and 2024. Still, with higher momentum from last year carrying over to 2023 and slightly better growth projected in the current quarter, by the end of the forecast horizon the volume of output is set to be almost 1 percent above that projected in autumn. Inflation is projected to end 2024 a notch above target, as in autumn.

While uncertainty surrounding the forecast remains high, risks to growth are broadly balanced. Domestic demand could turn out higher than projected, if the recent declines in wholesale gas prices pass through to consumer prices more strongly. Yet, a potential reversal of that fall cannot be ruled out in the context of Russia’s war against Ukraine and other geopolitical tensions. External demand could also turn out to be more robust following China’s re-opening, which could, however, fuel global inflation. Risks to inflation remain largely linked to developments in energy markets in the short run, but upside risks dominate in outer quarters, as a still tight labour market could result in stronger than anticipated wage pressure.

The EU economy beat expectations last year and we have entered 2023 on a firmer footing than anticipated. Yet Europeans still face a difficult period ahead with slowing growth and only gradually easing inflation.