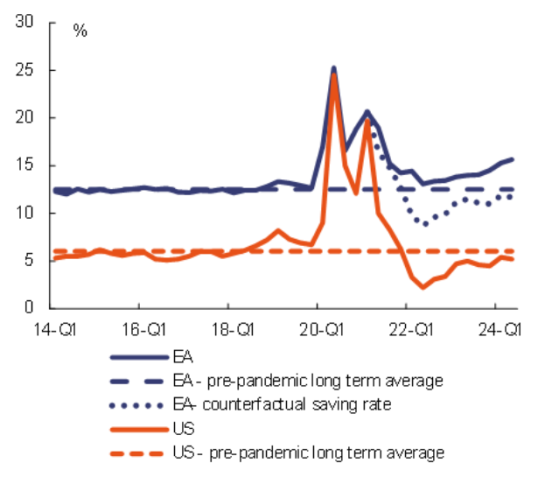

In the euro area (and the EU), the household saving rate has again been departing from its long-term average since mid-2022. As economies emerged from the pandemic, the saving rate started to reconverge towards its long-term average, falling from a peak of 20.6% in 2021-Q1 to 13.9% by 2022-Q2. However, the rapid surge in inflation and the forceful tightening of monetary conditions reversed this trend, pushing the saving rate up again to a high of 15.7% by 2024-Q2. The saving rate thus remained well above the pre-pandemic average of 12.3%.

By contrast, in the US, the saving rate has dipped below its long-term average. At the onset of the pandemic, the saving rate spiked also in the US, as consumers were forced to stay at home. Soon, however, US consumers started drawing on the extra savings accumulated during the pandemic. The US household saving rate fell to 2.2% in 2022-Q2, well below its 2014-19 average of 6.1%, even amid high inflation and interest rate hikes. It has since been creeping up, converging again to its long-term average.

| Graph 1: Household saving rate in the EA and in the US |

|

| Source: Eurostat for EA, Bureau of Economic Analysis for US. |

Higher saving rates in the euro area explain part of its weaker growth relative to the US. Two counterfactual analyses investigate the implications of the different saving behaviour in the US and the euro area. In a first “back-of-the-envelope" exercise, the deviation of the saving rate from its long-term average in the euro area is assumed to be the same as in the US, starting from 2021-Q1 (see Graph 1). In 2024-Q2, the euro area saving rate would be some 3 pps. below its actual reading. With no second-round effects, private consumption and GDP would have been on average 3.6% and 1.9% higher than observed between 2021-Q2 and 2024-Q2. An alternative model-based counterfactual exercise relying on the European Commission’s Global Multi-country (GM) (1) model identifies two domestic private demand forces that drive the divergence of the saving rate paths in the euro area and the US from 2021-Q3 until 2024-Q2. (2)

First, US households seem to have a more favourable attitude towards current spending than European consumers, as they tend to value spending today more than saving for the future. Second, the model estimates that the return on risky assets was lower than required by US savers, which further discouraged their savings propensity compared to the euro area. These two forces reduce the model-implied saving rate in the US by roughly 2 pps. on average during the observed period, in turn implying that GDP in the euro area would be 2.8% higher by end of 2024 – with part of the GDP increase would also result from stronger investment growth.