India’s importance in the global economy and as an economic partner to the EU is growing. Its share in the global economy, measured in purchasing power parity (PPP) terms, rose from 4% in 2000 to around 7.5% by 2023. IMF projections suggest that this share could rise to around 10% in 2030 ([1]). At global level, strong growth in India is projected to partially offset the slowdown in trend growth in China. India’s GDP per capita in PPP terms has increased more than fivefold since 2000, to USD 10,233 in 2023, though it remains at only 42% of that of China.

This special topic presents a snapshot of the Indian economy, highlighting its structural characteristics, recent developments, and the challenges that have so far hindered its deeper integration into the global economy. It also examines policy responses and explores India's economic relationship with the European Union. Starting in spring 2025, the forecast publications will include a specific country chapter on India and a more detailed forecast.

Structural features and challenges

India's economic history since independence in 1947 can be divided into two phases. The first phase, from 1947 to 1991, was characterized by a mixed economy model under the so-called "License Raj" system of strict government control and regulation, intended to protect Indian industry, promote self-reliance and ensure regional convergence. This period was characterised by moderate growth, averaging around 3.5% annually. The second phase began with the landmark economic reforms of 1991, triggered by a balance of payments crisis. These reforms ushered in an era of liberalisation, privatisation and globalisation that dismantled many of the restrictive economic policies. This shift led to significantly higher growth rates, averaging 6-7% annually, propelling India to become one of the world's fastest-growing major economies. The post-1991 period has seen the rise of India's IT and services sectors, substantial poverty reduction, and an expanding middle class, though challenges such as income inequality and infrastructure deficits persist. In particular, progress on poverty reduction has been patchy and in 2022 about 12% of Indians still lived on less than USD 2.15 per day.

| Graph II.2.1: GDP per capita in India and selected countries |

|

| Source: IMF |

India’s economic growth model stands out for its strong reliance on domestic consumption. The latter accounts for around 70% of its GDP, as the country's young, growing population has fuelled strong growth in internal demand. This consumption-driven growth model distinguishes India from many export-dependent economies, particularly in Asia. While it presents challenges, such as for managing inflation and trade deficits, it positions India favourably in the current global environment, by providing a buffer against external economic shocks and reducing vulnerability to international trade tensions and supply chain disruptions.

India’s economic development has quickly transitioned from a predominantly agrarian economy to one led by services. India’s economic development thus presents a potentially unique hybrid development model that combines a strong services sector with an emerging manufacturing base. However, many workers, especially those with limited education or skills, face barriers to securing quality jobs in the service sector and instead rely on self-employment or unpaid work, primarily in agriculture, construction and retail. These three sectors account for over half of total employment, and remain characterised by low productivity, limited value added and slow convergence to global productivity standards.

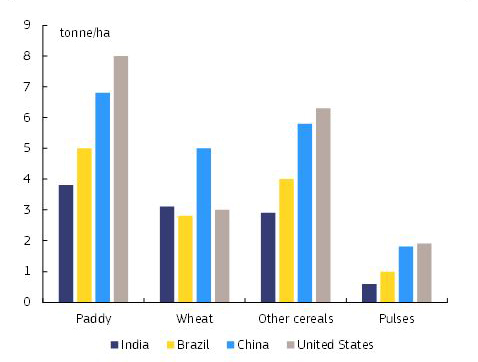

The agriculture and industry sectors exhibit low productivity and competitiveness. The agriculture sector, which still employs nearly half of India’s workforce, remains under-productive due to insufficient investment, outdated practices, and heavy dependence on government subsidies and price support schemes. Turning to the industrial sector, its share in GDP has declined almost uninterruptedly from 32.3% in 2011 to 27.6% in 2023, driven by the lagging manufacturing and mining sectors, undermined by poor infrastructure. In contrast to China, which accounted for 28.7% of global manufacturing output in 2021, India's share was only about 3.1%. Furthermore, India lags when it comes to integration in global manufacturing supply chains. Its widespread use of protectionist measures may impede the emergence of a strong manufacturing ecosystem, by limiting foreign direct investment (FDI) and integration into global value chains (GVC). Recently, the government's "Make in India" initiative and Production-Linked Incentive (PLI) schemes are actively promoting industrial growth, particularly in sectors like pharmaceuticals, automotive, and electronics.

| Graph II.2.2: Yields of cereals in India selected economies |

|

| Source: FAO. |

India’s population dynamics underpin its long-term economic potential. With a population estimated at 1.44 billion, in 2023 India became the world’s most populous country, surpassing China. According to UN projections ([2])(), India’s population will continue growing until mid-century to around 1.7 billion, offering a unique demographic dividend to the economy. A young and expanding workforce – if fully harnessed – could drive productivity improvements and growth in domestic consumption for many years, positioning India as a new engine of global economic growth.

At the same time, India faces important structural challenges that may limit its growth potential. Notwithstanding this demographic dividend, India has so far been unable to provide the sort of mass employment achieved in China. Approximately 90% of India’s workforce is engaged in informal employment ([3]), with many workers trapped in low-wage, insecure jobs that lack legal protection and benefits. Furthermore, women's participation in the workforce is exceedingly low, at approximately 26% in 2023, compared to a global average of around 47%. Furthermore, according to IMF estimates, India will need to generate between 145 and 330 million additional jobs by 2050 to meet the demands of its growing population. So far, capital deepening and productivity gains have accounted for the majority of growth, with little contribution from labour. The IMF estimates India’s medium-term potential growth at 6.3% ([4]), reflecting increased capital spending and a more robust labour market. Nevertheless, low overall productivity, a struggling manufacturing sector, a complex business environment, large labour market disparities, and the increasingly adverse effects of climate change may weigh on India’s growth potential if left unaddressed.

Climate change is emerging as a significant structural impediment to growth in India, characterised by prolonged periods of extreme temperatures, irregular precipitation and an increase in severe weather events. Over 75% of Indian districts are classified as hotspots for extreme climate events ([5]) and projections suggest that annual GDP losses due to extreme temperatures could reach 2.5-4.5% by 2030 ([6]). As one of the countries most vulnerable to climate change, and the third-largest CO2 emitter, India is committed to a low-carbon development path and has pledged to reach net zero emissions by 2070. However, significant investment will be required to enhance India’s climate resilience. India’s Ministry of Finance estimated a financing gap of USD 2.5 trillion (around 67% of India’s GDP) to meet India's nationally determined contribution (NDC) commitments by 2030 ([7]).

Recent economic developments

India emerged from the pandemic crisis as the fastest growing G20 economy. GDP growth averaged 6.5% in the 20 years before the pandemic. The Indian economy shrank by 6.6% during the first wave of COVID-19. The labour market suffered severe disruptions as the unemployment rate spiked, particularly in urban areas where informal workers and migrants were hardest hit, causing a notable increase in poverty levels. However, the economy rebounded quickly, registering an impressive 7.9% average growth rate since 2021. The key driver of India's post-pandemic recovery has been a surge in household consumption, which has grown by 7.8% per annum on average since 2021, boosted by improved labour market conditions, especially among casual workers. Investment grew by almost 12% per annum on average in the same period, supported by strong public investment in infrastructure. At the same time private sector investment has poured into sectors like real estate and manufacturing.

| Graph II.2.3: Contributions to global GDP growth |

|

| Source: IMF. |

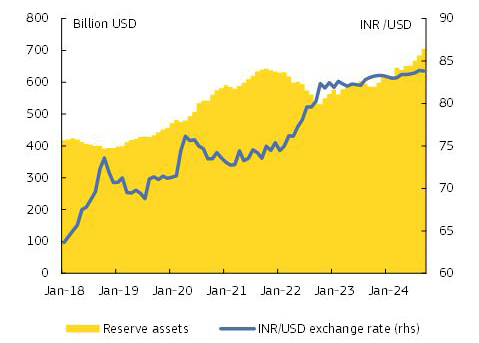

Inflation was quickly brought under control, thanks to prudent monetary policy. The Indian economy is particularly vulnerable to commodity price inflation. Driven by global food and energy price shocks along with supply chain disruptions, inflation peaked at 6.7% in 2022. The timely and aggressive tightening of monetary policy by the Reserve Bank of India (RBI) anchored inflation expectations and helped guide inflation back within the RBI’s tolerance band (2-6%). Inflation fell below the RBI target of 4% in July 2024, opening up potential space for monetary loosening. Monetary policy was also effective at managing depreciation pressures. After depreciating by 9.4% against the US dollar in 2022, the Rupee exchange rate movements moderated, which prompted the IMF to reclassify India’s de facto exchange rate regime from “floating” to a “stabilised arrangement”. India’s foreign exchange reserves stood at more than USD 700 billion in September 2024, covering more than 12 months worth of imports. With the exchange rate more tightly managed, ample reserves should help cushion the impact of external shocks going forward.

India’s fiscal position worsened considerably during the pandemic, but consolidation efforts have been ongoing since. Public debt shot up during the pandemic, from 74.3% of GDP in 2019-Q4, to 89.3% in 2021-Q1. It has since come down to around 83% of GDP. Debt sustainability risks are relatively contained. The bulk of public debt is in the form of rupee-denominated fixed-rate instruments of long maturity, predominantly held by residents. Still, fiscal risks remain present given past instances of fiscal slippages between 2000 and 2020, and India’s sensitivity to external shocks. The government budget deficit has come down since the pandemic and the new FY24 budget foresees further deficit reduction, with the authorities planning to achieve the central government deficit target of 4.5% of GDP by FY26.

India's financial sector has strengthened significantly in recent years, positioning it to support the country’s fast-growing economy and rising investment needs. After several years of slow credit growth, during which banks significantly improved their balance sheets, a new credit cycle began in mid-2021. Banks have reduced their non-performing loans (NPLs) from around 11% in 2018 to below 4% in 2023. Meanwhile, the average capital adequacy ratio has increased from below 13% to above 17% in 2023, comfortably above regulatory thresholds of 9% for commercial banks and 12% for publicly owned banks. As the financial sector strengthened its balance sheets, credit growth picked up markedly, from 8% in 2019 to almost 15% in 2025. Still, both household and corporate sector indebtedness remains moderate, at 42.7% and 55.8% of GDP in 2024-Q1 respectively.

| Graph II.2.4: India - monetary developments |

|

| Source: The Reserve Bank of India. |

India has been running a current account deficit almost uninterruptedly since 2000. The scale of deficits was mostly in line with fundamentals for a developing country in need of capital, and in most years were largely financed by flows of foreign direct investment. The current account deficit temporarily increased during 2022, to 2.4% of GDP from 1% in 2021, due to the energy price shock worsening India’s terms of trade. It has since come down to around 1% in 2023 and 2024-H1. Over the last 10 years, India’s national international investment position (NIIP) improved significantly. NIIP stood at -9.5% of GDP in H1 2024, up from -17.5% of GDP in 2014. At around 18.5% of GDP in 2024-H1, India’s external debt is low compared to peers. Furthermore, a large share of it is long term, limiting rollover risks.

Policy priorities and opportunities

The Indian government has been implementing a series of reforms to unlock the country's potential. One of the most significant initiatives is labour market reform. In 2020, the central government streamlined labour regulations by passing four major labour codes, with the aim to enhance labour flexibility, reduce regulatory complexity, and improve the conditions for formal employment. However, the implementation of these reforms at state level is lagging.

Investment in infrastructure is a key component of India’s development strategy. Public non-defence capital expenditure increased from 3.1% of GDP in FY19/20 to an estimated 4.9% of GDP in FY23/24, with both central and state governments increasing spending on infrastructure. For example, India doubled the number of airports over the past 10 years, and is adding 10 000 km of new roads and 15GW of solar-energy capacity each year ([8]). Nevertheless, there are still critical gaps, particularly in transport, energy and logistics, which limit access to markets and dampen growth. The focus on improving physical and digital infrastructure is therefore vital for increasing private sector productivity, to improve market access, and enhance India's global competitiveness.

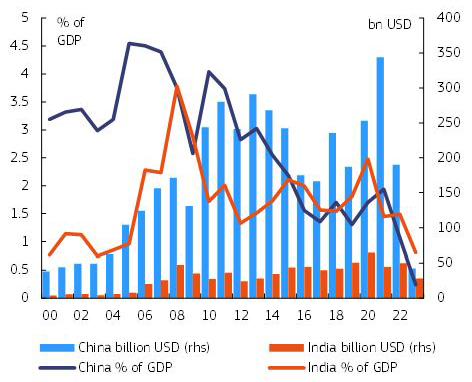

India is also working to promote exports and attract foreign direct investment. With global supply chains shifting due to geopolitical factors, India has an opportunity to benefit from the "friendshoring" trend, which involves relocating production to trusted countries. For example, global companies like Apple, Samsung and Foxconn have lately been expanding investment in new production capacities in India to diversify their supply lines. For the moment, most of their business in India is known as Final Assembly, Test and Pack (FATP), a low value added, labour-intensive process that assembles components largely imported from China. The government has introduced several initiatives, such as the Production-Linked Incentive (PLI) scheme, designed to attract foreign firms to establish manufacturing capacities in India, but also to incentivise them to go beyond establishing only FATP operations and encourage purchases of inputs in the domestic market. Furthermore, the authorities have recently been pursuing new trade agreements (e.g. with UAE and Australia) to complement existing export promotion policies and help increase bilateral trade and investment.

| Graph II.2.5: FDI inflows comparison between India and China |

|

| Source: Reserve Bank of India and National Bureau of Statistics of China. |

India’s growing digital economy presents another major opportunity. The country is already a global leader in information technology (IT) and business process management (BPM). The IT-BPM sector is projected to account for 10% of India’s GDP by 2025 and is highly export-oriented, with around 80% of its total revenue coming from abroad. Aside from price competitiveness, the IT industry in India benefits from a large number of skilled and English-speaking workers and the rapid expansion of digital infrastructure. India now hosts four of the world's top 100 science and technology clusters —Bengaluru, New Delhi, Mumbai, and Chennai ([9]). In recent years, India has also become the third largest source of startups globally, producing 118 unicorns with a combined value of over USD 350 billion.

EU-India economic relationship

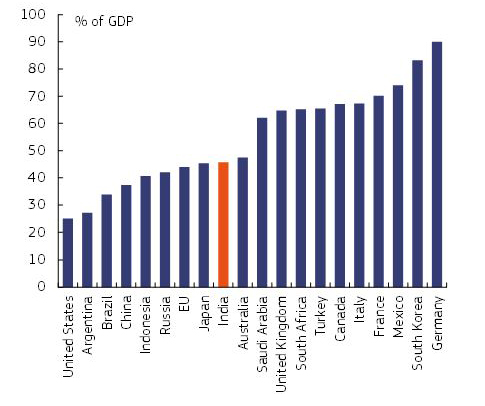

| Graph II.2.6: Trade openness |

|

| Source: WB WDI, IMF WEO. |

The European Union (EU) and India share a robust and growing economic relationship. The EU is India's largest trading partner, accounting for €124 billion worth of total trade in goods in 2023 or 12.2% of total Indian trade. India’s other major trade partners are USA (10.8% of total trade) and China (10.5%). However, India only accounts for 2% of the EU’s external trade and ranks as the 9th major EU trading partner. EU traders and investors continue to face many market access barriers on the Indian side, such as prohibitive import duties, sanitary and phytosanitary restrictions, and a growing number of technical barriers to trade. Despite these impediments, trade in goods between the EU and India has increased by almost 90% in the last decade, while in services it reached €50.8 billion in 2023, up from €30.4 billion in 2020. The EU is also a major source of FDI into India, particularly in the services sector, including telecommunications, financial and business services. The stock of EU’s direct investment in India reached EUR 108.3 billion in 2022, up from EUR 82.3 billion in 2019, making the EU a leading foreign investor in India. Yet, this is still below the EU’s foreign investment stocks in China (EUR 247.5 billion) or Brazil (EUR 293.4 billion).

There is substantial potential for further deepening EU-India economic ties. Ongoing negotiations (the 9th round of talks concluded in September 2024 in Delhi) for a Free Trade Agreement (FTA) hold promise for expanded trade in goods and services, as well as enhanced cooperation in key areas such as clean energy, smart cities and sustainable transportation. The FTA could help reduce trade barriers and align regulatory standards, providing opportunities for businesses on both sides to expand their operations. In recent years, the EU and India have also strengthened their cooperation in areas like climate change, sustainable development and the digital economy. As India moves toward a low-carbon development path, there is significant scope for collaboration in renewable energy, electric mobility and energy-efficient infrastructure.

Footnotes

([1]) Srivastava, D.K. (2022). “Indian economy by 2050: In pursuit to achieve the $30 trillion mark.” EY-India [Internet]

([2]) United Nations, Department of Economic and Social Affairs, Population Division (2024). World Population Prospects 2024: Data Sources. (UN DESA/POP/2024).

([3]) International Labour Organization (ILO) (2019), Informal Employment Trends in the Indian Economy: Persistent informality, but growing positive development, Working Paper No. 254

([4]) International Monetary Fund (IMF) (2023). India Article IV consultation, Washington DC: IMF, December.

([5]) Mohanty, Abinash (2020). “Preparing India for Extreme Climate Events: Mapping Hotspots and Response Mechanisms.” Council on Energy, Environment and Water.

([6]) McKinsey Global Institute (2020), “Will India get too hot to work?” Case study

([7]) Government of India, Ministry of Finance (2024), Economic Survey 2023-24. New Delhi, July

([8]) “How strong is India’s economy?,” The Economist, April 2023

([9]) World Intellectual Property Organization (WIPO) (2024). Global Innovation Index 2024 Unlocking the Promise of Social Entrepreneurship. Geneva: WIPO