Key figures

- GDP

EU:

2023: 0.4%

2024: 1.0%

2025: 1.6%Euro area:

2023: 0.4%

2024: 0.8%

2025: 1.4% - Inflation

EU:

2023: 6.4%

2024: 2.7%

2025: 2.2%Euro area:

2023: 5.4%

2024: 2.5%

2025: 2.1% - Deficit

EU:

2023: -3.5%

2024: -3.0%

2025: -2.9%Euro area:

2023: -3.6%

2024: -3.0%

2025: -2.8% - Unemployment

EU:

2023: 6.1%

2024: 6.1%

2025: 6.0%Euro area:

2023: 6.6%

2024: 6.6%

2025: 6.5%

Executive summary

The EU economy staged a comeback at the start of the year, following a prolonged period of stagnation. Though the growth rate of 0.3% estimated for the first quarter of 2024 is still below estimated potential, it exceeded expectations. Activity in the euro area expanded at the same pace, marking the end of the mild recession experienced in the second half of last year. Meanwhile, inflation across the EU cooled further in the first quarter.

This Spring Forecast projects GDP growth in 2024 at 1.0% in the EU and 0.8% in the euro area. This is a slight uptick from the Winter 2024 interim Forecast for the EU, but unchanged for the euro area. EU GDP growth is forecast to improve to 1.6% in 2025, a downward revision of 0.1 pps. from winter. In the euro area, GDP growth in 2025 is projected to be slightly lower, at 1.4% - also marginally revised down. Importantly, almost all Member States are expected to return to growth in 2024. With economic expansion in the southern rim of the EU still outpacing growth in north and western Europe, economic convergence within the EU is set to progress further. On the 20th anniversary of the enlargement of the EU towards the east and the south, it is notable that, after almost stalling last year, economic convergence is also set to resume for the newer Member States. It is expected to continue at a sustained pace throughout the forecast horizon and beyond (see Special Topic).

HICP inflation is projected to continue declining over the forecast horizon. In the EU, it is now expected to decrease from 6.4% in 2023 to 2.7% in 2024 and 2.2% in 2025. In the euro area, it is forecast to fall from 5.4% in 2023 to 2.5% in 2024 and 2.1% in 2025. This is a downward revision compared to winter for both the EU and the euro area – especially for this year.

Economic activity broadly stagnated in 2023. Private consumption only grew by 0.4%. Despite robust employment and wage growth, labour incomes barely outpaced inflation. Moreover, households put aside a larger share of their disposable incomes than in 2022, as high interest rates kept the opportunity cost of consumption elevated, while high uncertainty, the erosion of the real value of wealth by inflation and the fall in real estate prices sustained precautionary savings. Investment grew by 1.5% in 2023, but largely driven by a sizeable carry-over from 2022. Especially towards the end of the year, weakness in investment was widespread across Member States and asset types, with a pronounced downsizing of the interest-rate-sensitive construction sector. External demand did not provide much support either, weighed down by a sharp slowdown in global merchandise trade. Still, with domestic demand stagnating, imports contracted more than exports, lifting the contribution of net external demand to real GDP growth to a sizable 0.7 pps. Last, but not least, the negative drag of an unusually strong inventory cycle detracted almost 1 pp. from domestic demand, and explains most of the over-estimation of real GDP growth in 2023 in previous forecasts. Meanwhile, HICP inflation has continued declining. From a peak of 10.6% in October 2022, inflation in the euro area is estimated to have reached 2.4% in April 2024. Inflation in the EU followed a similar path, with the March reading (April was still missing at the cut-off date of this forecast) coming in at 2.6%. Rapid fall in retail energy prices throughout 2023 was the main driver of the inflation decline, but underlying inflationary pressures started easing too in the second half of 2023, amidst the weak growth momentum.

Expectations for imminent and decisive rate cuts across the world have been pared back in recent weeks, as underlying inflationary pressures - especially in the US – have proved more persistent than previously expected. In the euro area, where the European Central Bank last hiked its policy interest rates in September 2023, markets now expect a more gradual pace of policy rate cuts than in winter. Euribor-3 months futures suggest that euro area short-term nominal interest rates will decrease from 4% to 3.2% by the end of the year and to 2.6% by the end of 2025.

Outside the euro area, central banks in some central and eastern European countries, as well as Sweden (after the cut-off date) have already embarked on a cycle of monetary policy easing.

Although retail interest rates have already started to come down, bank lending has so far failed to rebound, due to some further tightening of credit standards, but especially lower corporate demand for loans. However, as interest rates keep falling, the conditions for a gradual expansion of investment activity remain in place and are even bolstered by the robust financial deleveraging in preceding quarters.

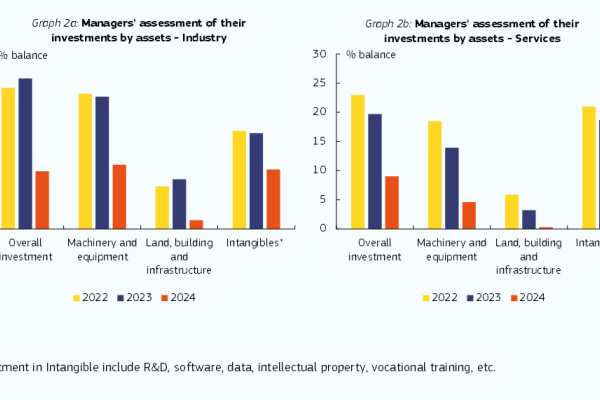

With prolonged weakness in the manufacturing sector leaving many plants operating below normal capacity utilisation rates, equipment investment is expected to expand only marginally this year (see Box I.2.1), before accelerating in 2025. Non-residential construction investment is expected to remain resilient, largely reflecting government infrastructure spending with RRF support. By contrast, housing investment is projected to continue contracting this as continued fall in house prices and a still large build-up of inventories weigh on supply. The downsize of residential construction is set to continue in 2025, but the aggregate outlook masks significant variation across countries.

Despite largely stagnant output, the EU economy created more than two million jobs in 2023, thanks to broad-based employment growth across the EU. According to the Labour Force Survey, the employment rate of people aged 20-64 in the EU hit the new record high of 75.5% in the last quarter of 2023.

Notwithstanding evidence of cooling demand, the labour market remains tight. In March the EU unemployment rate stood at its record low of 6.0%, and other measures of labour market slack remain near record-low levels. Furthermore, the unemployment rate continued falling in Member States recording the highest rates, resulting in continued decline of dispersion across countries. This strong labour market performance reflects favourable developments in both labour demand and labour supply, also due to migration. Going forward, the impulse of these positive drivers is set to abate, and employment growth is expected to be more subdued. Over the forecast horizon, however, the EU economy is still expected to generate another 2.5 million jobs, while the unemployment rate should hover around the current record-low rates. Nominal compensation per employee expanded by 5.8% in 2023 in the EU, with a gradual deceleration in the second half of the year. It is projected to decelerate further throughout the forecast horizon, alleviating underlying inflationary pressures. Importantly, growth in real wages – which started towards the end of last year – is set to continue throughout the forecast horizon. By 2025, average real wages are set to fully recover their 2021 levels, though this is not the case for all Member States.

Continued wage and employment growth will sustain growth in disposable income in 2024. A further uptick in the saving rate to 14.4% however limits the expansion of private consumption to 1.3% - still well below trend growth. In 2025, real disposable income is set to accelerate further, while the decline in interest rates reduces incentives to save. This is set to deliver a more sustained consumption growth, at 1.7% in the EU.

Despite facing headwinds from persistent inflation and restrictive monetary policies, growth outside of the EU remained resilient throughout 2023.

However, it failed to spur demand for EU exports. Factors such as the post-pandemic rotation of consumer demand from goods to services, inventory depletion in advanced economies, and tightened monetary conditions impacting trade-intensive capital goods together contributed to a significant downturn in global merchandise trade. In this lacklustre trade environment, the EU as a whole managed to gain export market shares, though some Member States continued to register important losses. Looking forward, global growth (excluding the EU) is set to remain at close to 3.5% over the forecast horizon. For the world as a whole, growth is projected to edge up from 3.1% in 2023 to 3.2% in 2024 and 3.3% in 2025. This is a marginally upward revision compared to the Winter Forecast. The growth outlook for the US looks better than previously expected, mainly on account of the strong end-of-2023 performance. The persistence of inflationary pressures, nevertheless, suggests that the drag of tight monetary conditions is set to continue in the short term.

Notwithstanding structural impediments (see Special Issue 4.2. China's impressive rise and its structural slowdown ahead: implications for the global economy and the EU), a strong rebound in China’s economic activity in the first quarter lifts its near-term outlook. Merchandise trade is set to rebound, as trade elasticity converges towards the “new normal” of around 1, below historical average. The improved outlook for global merchandise trade should support EU’s external demand for goods, in turn helping to lift the prospects of the weakened manufacturing sector. EU exports of goods and services are expected to expand by 1.4% this year and to attain 3.1% in 2025, amidst some losses in market shares. Imports are also set to rebound, implying a neutral or only marginally positive contribution to EU growth of net external demand in the two forecast years. With favourable movements in terms of trade, the current account balance of the EU is expected to rise back to 3.1% of GDP in both years, in line with pre-pandemic average, though with a larger contribution of export of services.

HICP inflation in the euro area is set to decrease from 5.4% in 2023 to 2.5% in 2024, while in the EU it is expected to decrease from 6.4% to 2.7%. Already by the end of last year, the disinflationary impulse of energy prices had largely died out. As recent increases in energy commodity prices – especially crude oil – are transmitted to consumers, energy inflation is set to turn positive again, but only marginally.

Food and non-energy industrial goods have now become the primary disinflation drivers and are expected to continue detracting from inflation over the forecast horizon, reflecting receding pipeline pressures. Service prices, in contrast, have so far contributed very little to the disinflation process, reflecting still elevated wage pressures. However, relatively weak economic momentum and decelerating wage growth should allow services inflation to ease over the forecast horizon. All in all, core inflation (excluding energy and food) is expected to decline over the forecast horizon at broadly the same pace as headline inflation, remaining just slightly above. After narrowing significantly since mid-2023, dispersion of inflation within the EU is set to decline further by 2025, reflecting country-specific drivers of core inflation, including the expected wage growth, developments in productivity and unit profits. These dynamics are largely mirrored by the GDP deflator – a measure of the evolution of domestic price pressures. The deflator is set to slowdown from 6% in 2023 to 3.3% in 2024 and 2.2% in 2025, as still high but abating wage growth is offset by a return to productivity growth and a reduction in profit margins.

After a sizeable reduction in 2022, the EU government deficit in 2023 increased marginally from 3.4% to 3.5% of GDP, as the deterioration economic conditions and increased interest expenditure outweighed the reduced cost of discretionary policy. The EU government deficit is nevertheless projected to resume declining in 2024 (to 3.0%) and 2025 (to 2.9%), driven by the almost complete phase-out of energy-related measures, lower subsidies on private investment as well as the gradual improvement in economic activity.

As in 2023, eleven Member States are projected to record a general government deficit exceeding 3% of GDP in 2024, dropping to nine in 2025. The EU fiscal stance turned neutral in 2023, after significant expansion in the 2020-22 period. It is set to be contractionary in 2024 and to turn broadly neutral in 2025.

This forecast incorporates all budgetary policies that have been adopted or credibly announced and sufficiently detailed (see Box 1.2.3). Amid higher costs of servicing debt and lower nominal GDP growth,

the debt-to-GDP ratio is set to stabilise this year, at 82.9% in the EU before edging up by around 0.4pps. in 2025. By the end of 2025, in most Member States the debt-to-GDP ratios are projected to be lower than in 2020 but to remain above 60% of GDP in 12 countries.

Risks originating from outside the EU have increased in recent months amid two ongoing wars in our neighbourhood and mounting geopolitical tensions. Global trade and energy markets appear particularly vulnerable. Moreover, persistence of inflation in the US may further delay rate cuts in the US, but also beyond, resulting in somewhat tighter global financial conditions. On the domestic front, EU Central Banks may also postpone rate cuts until the decline in services inflation firms. In addition, the need to reduce budget deficits and put debt ratios back on a declining path may require some Member States to pursue a more restrictive fiscal stance than currently projected for 2025, weighing on economic growth. At the same time, a decline in saving propensity could spur consumption growth, while residential construction investment could recover faster. Risks associated to climate change and the degradation of natural capital increasingly weigh on the outlook. The EU is particularly affected, as Europe is the continent experiencing the fastest increase in temperature.

The EU economy perked up markedly in the first quarter, indicating that we have turned a corner after a very challenging 2023. We expect a gradual acceleration in growth over the course of this year and next, as private consumption is supported by declining inflation, recovering purchasing power and continued employment growth. Government deficits should inch lower following the withdrawal of almost all energy support measures, but public debt is set to increase slightly next year, pointing to a need for fiscal consolidation while protecting investment. Our forecast remains subject to high uncertainty and – with two wars continuing to rage not far from home – downside risks have increased.

Documents

Special Issues - Spring 2024

Boxes - Spring 2024